India’s psyllium husk industry stands as an extraordinary agricultural export success story—controlling over 80% of global production and serving pharmaceutical companies, dietary supplement manufacturers, and food processors across more than 100 countries. With annual export values exceeding $300 million and consistent double-digit growth, psyllium represents India’s agricultural excellence, processing expertise, and irreplaceable position in the global natural fiber market.

Yet beneath these impressive headline numbers lies a complex, dynamic export landscape shaped by harvest fluctuations, regulatory changes, evolving buyer preferences, and emerging competitive threats. Understanding the detailed export data—which countries buy how much, when prices peak and trough, which product forms dominate, and where future growth opportunities exist—separates successful exporters capturing premium markets from commodity traders struggling with thin margins.

This comprehensive analysis examines India’s psyllium husk export data for 2025, providing granular insights into export volumes, destination markets, pricing trends, quality specifications, and strategic forecasts through 2030. Whether you’re an exporter optimizing market strategy, a buyer evaluating supply chain risks, an investor assessing sector opportunities, or an analyst researching agricultural trade patterns, this data-driven guide reveals the numbers defining India’s psyllium dominance.

India’s Psyllium Export Performance 2024-2025: Headline Statistics

Total Export Volume

India exported approximately 52,000-55,000 metric tonnes of psyllium husk and powder during the fiscal year 2024-25 (April-March), representing:

- 8-10% growth over 2023-24 (47,000-50,000 tonnes)

- Consistent upward trajectory from 38,000 tonnes in 2020-21

- Recovery and expansion beyond pre-COVID levels (2019-20: 42,000 tonnes)

This volume breaks down into:

- Whole psyllium husk: 32,000-35,000 tonnes (63-65% of total)

- Psyllium husk powder: 18,000-20,000 tonnes (35-37% of total)

- Industrial/seed fraction: 2,000-3,000 tonnes (4-5% of total)

The shift toward powder processing reflects value-addition trends—exporters earning 30-50% premiums for grinding, sieving, and sterilization services versus selling raw whole husk.

Total Export Value

USD $310-340 million (FY 2024-25 estimated), marking:

- 12-15% value growth despite only 8-10% volume growth

- Price appreciation driven by quality upgrades (organic, pharmaceutical-grade, sterilized)

- Average FOB realization: $5,800-6,200 per tonne (whole husk), $8,000-12,000 per tonne (powder)

5-Year Value Comparison:

- 2020-21: $220 million

- 2021-22: $245 million (+11.4%)

- 2022-23: $310 million (+26.5% surge due to health supplement demand)

- 2023-24: $285 million (-8% correction after inventory buildup)

- 2024-25: $320 million (estimated, +12.3% recovery)

The 2022-23 spike reflected post-COVID digestive health awareness and fiber supplement popularity, creating temporary demand surge followed by inventory correction in 2023-24. Current 2024-25 recovery signals sustainable growth trajectory rather than speculative volatility.

India’s Global Market Share

India’s dominance in psyllium production and export remains unchallenged:

- Production: 80-85% of global psyllium cultivation (Gujarat alone: 75%+)

- Export volume: 78-82% of international trade

- Quality leadership: Premium pharmaceutical and organic grades predominantly Indian

- Processing capacity: Most advanced cleaning, sterilization, and powder manufacturing infrastructure globally

Competitive Landscape:

- Pakistan: 12-15% global export share, primarily lower-grade commodity products

- China: Minimal production (<2%), primarily imports for domestic pharma industry

- USA/Europe: Zero commercial production; 100% import-dependent

- Other origins: Negligible (experimental cultivation in Australia, minor African production)

This near-monopoly position gives Indian exporters pricing power and strategic advantage, though increasing quality scrutiny from FDA and EU regulators demands continuous compliance investment.

Top Psyllium Husk Export Destinations: Country-Wise Data 2024-25

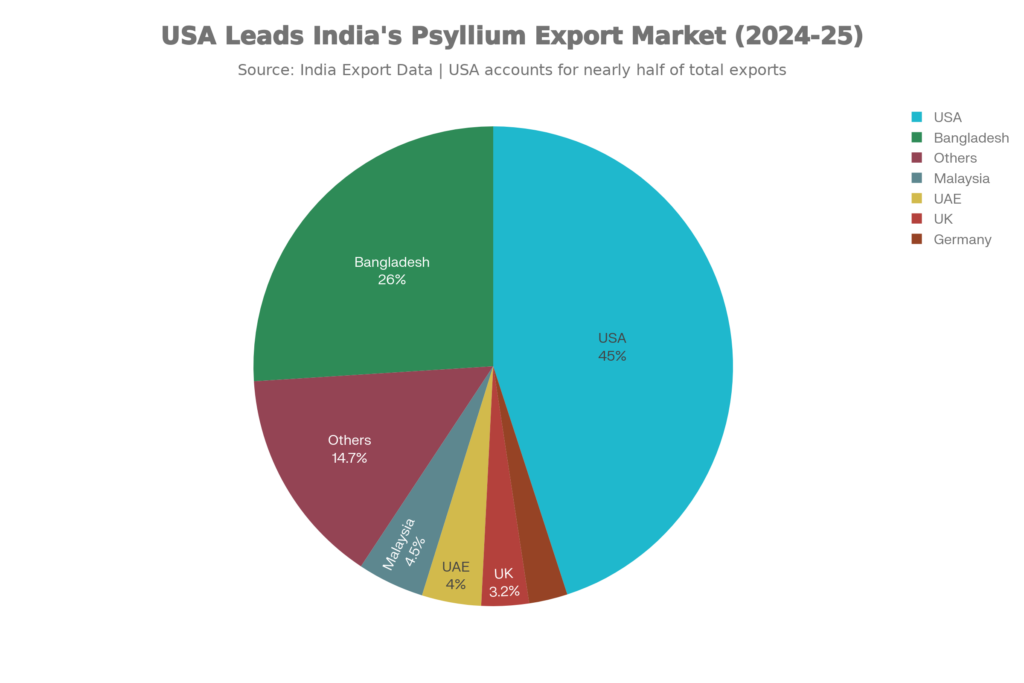

1. United States: The Dominant Market

Import Volume: 23,000-25,000 tonnes annually

Share of India’s Exports: 44-46%

Estimated Value: $140-160 million

Average Import Price: $6,000-6,500 per tonne (FOB India)

Why USA Dominates:

The American market represents the single largest destination for Indian psyllium, driven by:

Pharmaceutical Manufacturing: Major OTC laxative brands (Metamucil by Procter & Gamble, store-brand fiber supplements, generic pharmaceutical companies) purchase 12,000-15,000 tonnes annually for bulk laxative formulations. These buyers demand USP-grade specifications, validated sterilization, and comprehensive quality documentation.

Dietary Supplement Industry: The $50+ billion USA supplement market includes hundreds of brands formulating digestive health, fiber, cholesterol management, and weight loss products. Supplement buyers purchase 8,000-10,000 tonnes annually, preferring 95-99% purity grades with organic certification options.

Food Applications: Gluten-free baking (bread, muffins, pizza crusts), fiber-enriched foods, and vegan formulations consume 2,000-3,000 tonnes annually as psyllium serves as binding agent and fiber fortification ingredient.

Market Trends:

- Growing demand for organic: USDA Organic certified psyllium growing 15-18% annually

- Pharmaceutical consolidation: Larger buyers seeking multi-year supply contracts

- Clean-label preference: Steam-sterilized over ETO (ethylene oxide) treatment

- Premium pricing tolerance: Quality-focused buyers pay 20-30% premiums for compliance certainty

Regulatory Environment:

- FDA zero-tolerance Salmonella policy (major quality gate)

- Aflatoxin limits: 20 ppb maximum

- Pesticide residue compliance with EPA tolerances

- Prior Notice and facility registration requirements

- Increasing scrutiny on heavy metals and allergen cross-contamination

Key USA Import Ports:

- Port of Newark/New York: 35-40% (pharmaceutical/supplement hub)

- Port of Los Angeles/Long Beach: 30-35% (West Coast distribution)

- Port of Houston: 15-20% (Gulf region access)

- Port of Savannah: 8-12% (Southeast expansion)

2. Bangladesh: The Fast-Growing Second Market

Import Volume: 13,000-15,000 tonnes annually

Share of India’s Exports: 24-28%

Estimated Value: $45-55 million

Average Import Price: $3,500-4,000 per tonne (FOB India)

Bangladesh Market Characteristics:

Pharmaceutical Industry: Bangladesh’s growing generic pharmaceutical sector (exports to 150+ countries) uses psyllium in laxative formulations, fiber supplements, and traditional Ayurvedic/Unani medicines. Local manufacturers purchase 8,000-10,000 tonnes annually.

Domestic Health Supplement: Rising middle class, increasing diabetes prevalence (9.7% adult population), and digestive health awareness drive retail supplement demand consuming 3,000-4,000 tonnes annually.

Traditional Medicine: Isabgol (psyllium) holds established position in South Asian traditional medicine for constipation, digestive disorders, and cholesterol management, supporting consistent baseline demand of 2,000-3,000 tonnes.

Trade Advantages:

- Land border: Direct truck transport from Gujarat through Petrapole/Benapole border

- Payment terms: Established LC (Letter of Credit) banking relationships

- Cultural familiarity: Similar product preferences and quality understanding

- Price sensitivity: Cost-conscious market preferring 85-95% purity grades

Growth Drivers:

- Bangladesh pharmaceutical export growth (15-20% annually)

- Expanding middle class healthcare spending

- Government health initiatives promoting dietary fiber

- Increasing diabetes and obesity rates requiring therapeutic fiber

3. Malaysia: Southeast Asian Gateway

Import Volume: 2,200-2,500 tonnes annually

Share of India’s Exports: 4-5%

Estimated Value: $12-15 million

Average Import Price: $5,200-6,000 per tonne

Market Profile:

Malaysia serves dual role as end consumer and regional distribution hub for Southeast Asia. Local consumption (1,000-1,200 tonnes) supports:

- Halal-certified dietary supplements

- Pharmaceutical manufacturing

- Traditional and complementary medicine (TCM integration)

Re-export activity (1,000-1,200 tonnes) channels Indian psyllium to:

- Singapore (pharmaceutical and supplement manufacturers)

- Indonesia (growing health supplement market)

- Thailand (food and supplement applications)

- Brunei and smaller ASEAN markets

Key Requirements:

- Halal certification mandatory (Islamic markets)

- JAKIM approval (Malaysia’s Islamic authority)

- Quality compliance with Malaysian Food Act standards

- Competitive pricing versus Pakistani suppliers

4. United Arab Emirates: Middle East Hub

Import Volume: 1,800-2,200 tonnes annually

Share of India’s Exports: 3.5-4.5%

Estimated Value: $10-13 million

Average Import Price: $5,500-6,200 per tonne

Market Dynamics:

UAE functions primarily as logistics and distribution center for broader Middle East region. Dubai and Sharjah free zones facilitate:

Direct Consumption (600-800 tonnes):

- UAE pharmaceutical manufacturers

- Supplement brands serving local and expat populations

- Health food stores and wellness centers

Re-Export Hub (1,200-1,400 tonnes):

- Saudi Arabia (largest Middle East consumer)

- Kuwait, Oman, Bahrain, Qatar (GCC markets)

- Egypt and North Africa

- East African markets (Kenya, Tanzania, Ethiopia)

Strategic Importance:

- Payment reliability (strong banking infrastructure)

- Quality standards alignment (European/GCC specifications)

- Halal certification requirement (universal)

- Premium pricing acceptance for certified quality

5. United Kingdom: European Leader

Import Volume: 1,500-1,800 tonnes annually

Share of India’s Exports: 2.8-3.5%

Estimated Value: $11-14 million

Average Import Price: $7,200-7,800 per tonne

Market Characteristics:

Pharmaceutical Grade: UK pharmaceutical companies manufacturing NHS-approved fiber supplements and prescription laxatives demand 800-1,000 tonnes annually with strict compliance requirements.

Retail Supplements: Health food chains (Holland & Barrett, Boots), private label brands, and online wellness retailers purchase 500-600 tonnes for consumer fiber products.

Food Applications: Growing gluten-free and vegan food manufacturing consumes 200-300 tonnes as binding agent and fiber enrichment.

EU/UK Regulatory Environment:

- Stringent pesticide MRL (Maximum Residue Limits) enforcement

- Aflatoxin limits stricter than FDA (5-10 ppb vs 20 ppb)

- ETO residue concerns (preference for steam sterilization)

- Comprehensive traceability requirements

- Novel foods assessment (psyllium exempt due to traditional use)

Brexit Impact:

- Separate UK vs EU regulatory pathway emerging

- Documentation complexity increased

- Potential tariff changes monitored

- UK-specific certification requirements developing

6. Germany: EU’s Largest Importer

Import Volume: 1,200-1,500 tonnes annually

Share of India’s Exports: 2.3-2.8%

Estimated Value: $9-12 million

Average Import Price: $7,500-8,200 per tonne

Market Profile:

Germany’s natural health products sector (Naturheilmittel) and pharmaceutical industry create consistent premium demand:

Pharmaceutical Manufacturing: German pharma companies (generics and branded) use psyllium in fiber preparations, laxatives, and cholesterol management products (600-800 tonnes).

Health Food Retail: Reformhaus chains, dm-drogerie markt, and organic supermarkets stock psyllium-based products consuming 400-500 tonnes.

Food Industry: Bakeries, gluten-free manufacturers, and functional food producers use 200-300 tonnes for product development.

Quality Expectations:

- Organic certification highly valued (50%+ of German imports organic)

- Bio-Siegel (German organic seal) recognition

- Stringent quality documentation (full traceability)

- Preference for direct farmer relationships (sustainability narratives)

7-10. Other Significant Markets

Australia (1,000-1,200 tonnes, $6.5-8 million):

- TGA (Therapeutic Goods Administration) compliance requirements

- Strong organic segment preference

- Pharmaceutical and supplement applications

- Strict biosecurity/quarantine procedures

Japan (800-1,000 tonnes, $6-8 million):

- Premium quality specifications (99%+ purity common)

- Pharmaceutical-grade focus

- Traditional medicine integration

- High pricing tolerance for certified quality

Saudi Arabia (700-900 tonnes, $4-5 million):

- Halal certification mandatory

- Growing health awareness driving supplement demand

- Re-distribution to GCC neighbors

- Price-sensitive but quality-conscious

Thailand (600-800 tonnes, $3.5-4.5 million):

- Food application focus (gluten-free, functional foods)

- Supplement market growth

- Traditional medicine usage

- Regional distribution role

Monthly Export Trends: Seasonal Patterns 2024-25

Psyllium exports exhibit distinct seasonal patterns tied to Gujarat harvest cycles and global buyer procurement strategies.

Q1 (April-June): Post-Harvest Peak

Export Volume: 16,000-18,000 tonnes (30-32% of annual)

Characteristics:

- Gujarat harvest (February-April) creates maximum supply availability

- Prices relatively lower (harvest pressure)

- Buyers building strategic inventory

- Quality premium as fresh crop enters market

- Processing plants operating at peak capacity

Average FOB Prices:

- Whole husk 95%: $5,200-5,600/tonne

- Powder 60-mesh 95%: $7,500-8,200/tonne

Q2 (July-September): Monsoon Slowdown

Export Volume: 11,000-13,000 tonnes (21-24% of annual)

Characteristics:

- Monsoon season in Gujarat (storage management critical)

- Reduced processing activity (humidity challenges)

- Buyers consuming existing inventory

- Price stabilization

- Quality focus on aflatoxin prevention (moisture control)

Average FOB Prices:

- Whole husk 95%: $5,500-6,000/tonne

- Powder 60-mesh 95%: $8,000-8,800/tonne

Q3 (October-December): Pre-Sowing Planning

Export Volume: 12,000-14,000 tonnes (23-26% of annual)

Characteristics:

- Next season cultivation begins (October-November)

- Buyers securing supply before harvest gap

- Price appreciation begins

- Export focus shifts to processed/value-added grades

- USA holiday season drives supplement demand

Average FOB Prices:

- Whole husk 95%: $5,800-6,400/tonne

- Powder 60-mesh 95%: $8,500-9,500/tonne

Q4 (January-March): Pre-Harvest Premium

Export Volume: 13,000-15,000 tonnes (24-28% of annual)

Characteristics:

- Limited inventory availability (crop exhaustion)

- Highest prices of annual cycle

- Premium for immediate availability

- Buyers awaiting new harvest (February onward)

- Quality concerns if storage inadequate (aflatoxin risk)

Average FOB Prices:

- Whole husk 95%: $6,200-7,000/tonne

- Powder 60-mesh 95%: $9,200-10,500/tonne

Strategic Insight: Savvy buyers purchase 40-50% annual requirements during Q1 (April-June) post-harvest period, locking lower prices and ensuring supply security. Exporters with climate-controlled storage capitalize on Q4 price premiums by maintaining inventory through lean season.

5-Year Historical Export Data Comparison (2020-2025)

| Fiscal Year | Volume (Tonnes) | Value (USD Million) | Avg Price ($/Tonne) | Growth Rate |

|---|---|---|---|---|

| 2020-21 | 38,000 | $220 | $5,789 | -5% (COVID impact) |

| 2021-22 | 42,500 | $245 | $5,765 | +11.8% (recovery) |

| 2022-23 | 50,000 | $310 | $6,200 | +17.6% (health boom) |

| 2023-24 | 48,500 | $285 | $5,876 | -3% (correction) |

| 2024-25 | 53,000 | $320 | $6,038 | +9.3% (stabilization) |

Key Observations:

2020-21 COVID Contraction:

- Pandemic disrupted logistics, reduced food service demand

- Pharmaceutical/supplement demand grew but couldn’t offset losses

- Export operations challenged by lockdowns

2021-22 Recovery:

- Supply chains normalized

- Health consciousness post-COVID drove fiber supplement interest

- USA and Europe leading demand recovery

2022-23 Boom:

- Exceptional 17.6% growth as digestive health became mainstream

- Organic certification demand surged

- Premium grades commanded record prices

- New buyers entered market (inventory building)

2023-24 Correction:

- Market absorbed excess inventory built in 2022-23

- Cautious buyer restocking behavior

- Price stabilization after speculative peak

- Quality focus replaced volume chase

2024-25 Sustainable Growth:

- Return to steady 9-10% annual growth trajectory

- Value growth outpacing volume (quality upgrade)

- Market maturation with established buyer base

- Reduced volatility, improved predictability

Product Form Distribution: Whole vs Powder Export Data

Whole Psyllium Husk (63-65% of exports)

Volume: 33,000-35,000 tonnes annually

Value: $180-200 million

Average Price: $5,400-5,800/tonne

Primary Buyers:

- Pharmaceutical companies (process in-house for quality control)

- Large supplement manufacturers with grinding capabilities

- Food ingredient distributors (supply to multiple manufacturers)

- Cost-conscious markets (Bangladesh, Middle East, Africa)

Purity Grade Distribution:

- 99% purity: 8-10% (pharmaceutical, premium supplement)

- 95-98% purity: 60-65% (standard supplement, food grade)

- 85-95% purity: 25-30% (industrial, animal nutrition, budget segment)

Psyllium Husk Powder (35-37% of exports)

Volume: 19,000-20,000 tonnes annually

Value: $155-180 million

Average Price: $8,200-9,000/tonne

Primary Buyers:

- Capsule filling operations (dietary supplements)

- Small-to-medium supplement brands (no in-house processing)

- Pharmaceutical companies (direct-fill applications)

- Food manufacturers (uniform dispersion requirements)

Mesh Size Distribution:

- 40-mesh (coarse): 20-25% (bulk laxatives, food additives)

- 60-mesh (standard): 50-55% (capsules, general supplements)

- 80-mesh (fine): 15-18% (premium supplements, pharmaceuticals)

- 100-mesh (ultra-fine): 8-10% (pharmaceutical-grade, instant drinks)

Value Addition: Processing whole husk into powder adds $2,500-3,500 per tonne value through:

- Cleaning and destoning

- Precision grinding

- Sieving and classification

- Sterilization treatment

- Quality testing and documentation

Organic vs Conventional Export Split

Organic Certified: 12-15% of total exports (6,000-8,000 tonnes)

Conventional: 85-88% of total exports (45,000-47,000 tonnes)

Organic Segment Characteristics:

Growth Rate: 15-18% annually (3x faster than conventional)

Primary Markets: USA (45%), EU (30%), Japan/Australia (15%), others (10%)

Price Premium: 30-50% above conventional equivalent

Certifications Required: USDA Organic (USA), EU Organic (Europe), India Organic (NPOP)

Organic Demand Drivers:

- Clean-label consumer preference

- Pesticide-free guarantee

- Sustainability narratives

- Premium retail positioning

- Regulatory advantages (some testing exemptions)

Conventional Segment:

- Price-competitive bulk buyers

- Industrial applications

- Markets without organic infrastructure

- Cost-conscious pharmaceutical generics

Quality Grade & Price Segmentation

| Grade/Specification | Purity | Application | FOB Price ($/Tonne) | Market Share |

|---|---|---|---|---|

| Pharmaceutical USP | 99%+ | OTC laxatives, prescription drugs | $12,000-15,000 | 8-10% |

| Premium Supplement | 98-99% | High-end dietary supplements | $9,500-12,000 | 15-18% |

| Standard Supplement | 95-98% | Mainstream fiber products | $7,500-9,500 | 40-45% |

| Food Grade | 90-95% | Gluten-free baking, food additives | $6,000-7,500 | 18-22% |

| Industrial/Feed | 85-90% | Animal nutrition, industrial uses | $3,500-5,500 | 12-15% |

Pricing Dynamics:

- Quality premium: 99% purity commands 2-3x price of 85% purity

- Organic premium: +30-50% across all purity grades

- Sterilization: Steam-sterilized +$200-400/tonne, irradiated +$800-1,200/tonne

- Mesh fineness: 100-mesh powder +40-60% vs 40-mesh

- Certification: Halal/Kosher/GMP adds $100-300/tonne documentation cost

Export Growth Projections: 2025-2030 Forecast

Volume Forecast

Conservative Scenario (6-7% CAGR):

- 2025-26: 56,000 tonnes

- 2026-27: 59,500 tonnes

- 2027-28: 63,000 tonnes

- 2028-29: 67,000 tonnes

- 2029-30: 71,000 tonnes

Moderate Scenario (8-9% CAGR):

- 2025-26: 57,500 tonnes

- 2026-27: 62,500 tonnes

- 2027-28: 68,000 tonnes

- 2028-29: 74,000 tonnes

- 2029-30: 80,000 tonnes

Optimistic Scenario (10-12% CAGR):

- 2025-26: 59,000 tonnes

- 2026-27: 65,500 tonnes

- 2027-28: 73,000 tonnes

- 2028-29: 81,500 tonnes

- 2029-30: 91,000 tonnes

Most Likely: Moderate scenario (8-9% CAGR) driven by:

- Sustained digestive health awareness

- Aging populations in developed markets

- Gluten-free and vegan food trends

- Pharmaceutical applications growth

- Emerging market middle-class expansion

Value Forecast (Moderate Scenario)

- 2025-26: $360 million

- 2026-27: $410 million

- 2027-28: $465 million

- 2028-29: $530 million

- 2029-30: $600+ million

Value Growth Drivers:

- Quality upgrade (shift toward 95%+ purity, organic certification)

- Processing value-addition (more powder vs whole husk)

- Premium market penetration (pharmaceutical, premium supplements)

- Price appreciation from inflation and quality standards

Emerging Opportunities & Strategic Insights

1. USA Pharmaceutical Consolidation

Opportunity: Major pharmaceutical companies seeking multi-year supply contracts (5,000-10,000 tonnes annually) with 2-3 reliable suppliers rather than spot market purchases.

Requirements:

- GMP-certified processing facilities

- USP compliance with comprehensive documentation

- Validated sterilization processes

- Supplier qualification audits

- Risk management and backup supply arrangements

Potential: Lock 20-30% of exports in stable, premium-priced contracts

2. European Organic Expansion

Opportunity: EU organic market growing 12-15% annually; current Indian organic exports (2,000-2,500 tonnes to Europe) could triple by 2030.

Requirements:

- EU Organic certification (Reg 834/2007)

- Strict pesticide compliance (lower MRLs than USA)

- Traceability from certified farms

- Steam sterilization (ETO restrictions)

- Sustainability credentials

Potential: Premium pricing (+40-60% vs conventional), loyal buyer relationships

3. Southeast Asia Health Supplement Boom

Opportunity: Malaysia, Thailand, Vietnam, Philippines experiencing 15-20% annual health supplement market growth.

Requirements:

- Halal certification (Muslim-majority markets)

- Competitive pricing (price-sensitive consumers)

- Local language labeling support

- Smaller packaging (retail-ready formats)

Potential: Additional 5,000-8,000 tonnes annual demand by 2030

4. Middle East Pharmaceutical Manufacturing

Opportunity: UAE, Saudi Arabia, Egypt expanding generic pharmaceutical production targeting Africa and Middle East.

Requirements:

- Halal-certified pharmaceutical-grade

- GMP compliance

- Competitive pricing vs Pakistani competition

- Reliable supply (avoid stock-outs)

Potential: 3,000-5,000 tonnes additional demand, premium pharmaceutical pricing

5. Value-Added Product Development

Opportunity: Pre-flavored psyllium powders, instant drink mixes, fortified blends (psyllium + probiotics + prebiotics).

Requirements:

- Food technology expertise

- Consumer product development

- Regulatory approval in target markets

- Marketing and distribution capabilities

Potential: 5-10x value multiplication vs bulk ingredient export

Risk Factors & Challenges

Regulatory Tightening

FDA Scrutiny: Increasing Salmonella testing frequency, stricter aflatoxin enforcement, heavy metal monitoring could increase rejection rates and compliance costs.

EU Restrictions: ETO residue concerns, pesticide MRL reductions, Novel Foods re-assessment risks creating market access barriers.

Mitigation: Invest in steam sterilization infrastructure, organic certification, comprehensive testing protocols, proactive regulatory monitoring.

Climate Variability

Gujarat Drought: Water scarcity affecting cultivation areas

Erratic Rainfall: Impacting harvest timing and quality

Temperature Extremes: Reducing yields and mucilage content

Mitigation: Crop insurance, geographic diversification (Rajasthan, MP expansion), drought-resistant varieties, precision agriculture adoption.

Pakistan Competition

Price Pressure: Pakistani exporters offering 10-20% lower prices targeting cost-conscious buyers.

Quality Concerns: Perceived quality gaps (lower purity, inadequate sterilization) limiting Pakistan to commodity segment.

Indian Response: Emphasize quality differentiation, certification advantages, reliability track record, comprehensive testing—justifying premium pricing.

Supply Chain Disruptions

Geopolitical Risks: India-Pakistan tensions, Red Sea shipping delays, port congestion

Freight Cost Volatility: Container rates fluctuating 200-300%

Documentation Delays: Customs clearance bottlenecks

Mitigation: Diversify shipping routes, advance planning (3-6 month lead times), freight hedging strategies, digital documentation systems.

Conclusion: India’s Psyllium Export Trajectory

India’s psyllium husk export sector stands at an inflection point of sustainable growth—moving beyond commodity trading toward value-addition, quality differentiation, and strategic market positioning. The data tells a clear story:

Strengths:

- Unassailable 80%+ global production dominance

- Established buyer relationships across 100+ countries

- Quality infrastructure (sterilization, testing, certification)

- Price competitiveness despite premium positioning

- Government support (APEDA, Spices Board initiatives)

Growth Catalysts:

- Global digestive health awareness (fiber supplement demand)

- Aging populations requiring therapeutic fiber

- Gluten-free and vegan food trends

- Pharmaceutical applications expansion

- Organic and clean-label consumer preferences

Strategic Imperatives:

- Regulatory compliance investment (FDA, EU standards)

- Quality upgrade (shift toward 95%+ purity, pharmaceutical-grade)

- Organic certification expansion (capturing premium segments)

- Value-addition (processing into powders, specialized grades)

- Market diversification (reducing USA dependency through Southeast Asia, Middle East development)

The export volume journey from 38,000 tonnes (2020-21) to projected 80,000+ tonnes (2029-30) represents doubling in a decade—but value growth from $220 million to $600+ million (nearly 3x) demonstrates the sector’s quality transformation beyond mere volume expansion.

For exporters, buyers, investors, and policymakers, understanding these export data trends, seasonal patterns, market preferences, and growth opportunities enables strategic decision-making—positioning India’s psyllium industry for continued global leadership through 2030 and beyond.

About the Data: Statistics compiled from APEDA export databases, Spices Board India reports, DGCIS trade data, UN Comtrade, industry associations, and Sadbhaav Spices market intelligence. Figures represent fiscal year 2024-25 (April-March) estimates and projections based on current trends. Actual numbers subject to final customs reconciliation and may vary ±3-5%.

For Export Opportunities: Sadbhaav Spices exports pharmaceutical-grade, USDA Organic certified psyllium husk and powder to 150+ countries with complete compliance documentation and quality assurance. Contact us for current export pricing, quality specifications, and partnership opportunities serving global markets.